Another month has FLOWN by – time for another mortgage market update!

April 06: The Employment Report for the previous month was released. Employment remained strong and (most troubling to the Bank of Canada), was that wage inflation also remained strong. Keep in mind that the jobs market is a lagging indicator and so the central bank will be watching the next few reports very closely.

April 12: Another Bank of Canada meeting was held to determine whether or not to change their overnight lending rate. Good news for all of us with variable rate mortgages: there will be no change to the prime rate. As of today, the prime rate remains at 6.70%. The next meeting is scheduled for June 07, 2023.

The Bank of Canada is so far expected to hold off on rate hikes in the near future, although rest assured that the rates will not be dropping until late 2023 or even possibly not until 2024. The Governor of the Bank of Canada has reiterated that rates must remain restrictive in order for inflation to continue the downward trend and return to target.

April 18: The last time that I touched base with you, headline inflation was sitting at 5.2%. The March CPI (Consumer Price Index) report was recently released and inflation has fallen to 4.3%. This is encouraging news after a tough 2022 with rising inflation. Having said that, all Canadians are still feeling the effects of high consumer goods pricing; particularly at the grocery store. The prices on food have increased once again year over year; however, the increase is at a slower pace – let’s hope that this continues!

New Program Launched for First-Time Home Buyers:

The Government of Canada has another program that gives First-time Home Buyers more tax breaks to build a down payment. This is called the First Home Savings Account. Rob McLister, with MortgageLogic News, has broken it down for us simply:

- You must be a first-time home buyer as per the federal definition (let me know if you have questions regarding the definition and whether you fit in this category)

- You can save up to $8,000 per year ($40,000 per lifetime)

- Contributions are tax-deductible, much like an RRSP

- Gains AND withdrawals are tax-free if used to purchase a qualifying principal residence.

- The funds do NOT have to be repaid; this separates the FHSA from the existing Home Buyers’ Plan using your RRSPs.

Looking for more information on this? Click the link here: CRA – FHSA

Note: This is general information that’s subject to change. It’s provided as-is and is not meant to be advice, including but not limited to tax, legal or investing advice. Caveats apply to some of the points mentioned. Readers should consult a tax professional for guidance applicable to their circumstances.

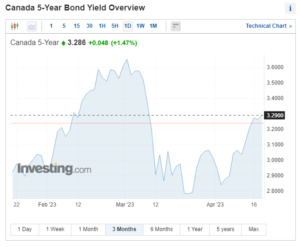

Canadian Bond Market:

The bond yields have been an absolute roller coaster ride this year so far. Bond yields have an effect on fixed mortgage rates and what lenders offer at any given time. Late March and early April saw yields decline. With those declines, some lenders (not all) began to slowly reduce fixed rate offerings. Those lower rates may not be here to stay as the bond yields continue to creep back up (see the 3-month chart below). When you are researching rates online, there are several important points to keep in mind:

- Insured rates (higher than 80% loan-to-value) will always be lower.

- Make sure the rate offering is not for a mortgage product with limitations

- Shorter terms (1-4 years) are higher – sometimes much higher – than a 5 year fixed rate option

- Refinance rates are higher than the rates offered for a purchase, in most cases.

As always, I will keep you up to date on the mortgage market each month. Do not hesitate to reach out with any questions, I am happy to help.

Happy Spring to you all